Housing Affordability Rebound: How Falling Mortgage Rates Unlock First-Time Buyers

The 2026 housing market is experiencing a gradual affordability rebound as mortgage rates decline from their recent peaks, creating new opportunities for first-time buyers

Last updated: February 24, 2026

The 2026 housing market is experiencing a gradual affordability rebound as mortgage rates decline from their recent peaks, creating new opportunities for first-time buyers who have been sidelined for years. While rates remain in the low-6% range as of early 2026, the shift from 7%+ rates in previous years is expanding buyer purchasing power and reshaping market dynamics across the country.

Key Takeaways

- Mortgage rates dropped to the low-6% range in early 2026, down from 7%+ peaks, with sustained sub-6% rates expected by 2027[2]

- Income required to buy a median-priced home fell from $103,000 to $94,000 year-over-year, signaling gradual affordability improvement[1]

- Each 1% rate drop can increase buying power by roughly 10-12%, allowing buyers to afford homes priced $30,000-$50,000 higher at the same monthly payment

- Inventory increased 15.2% in 2025 with another 8.9% growth expected in 2026, giving buyers more negotiating leverage[1][2]

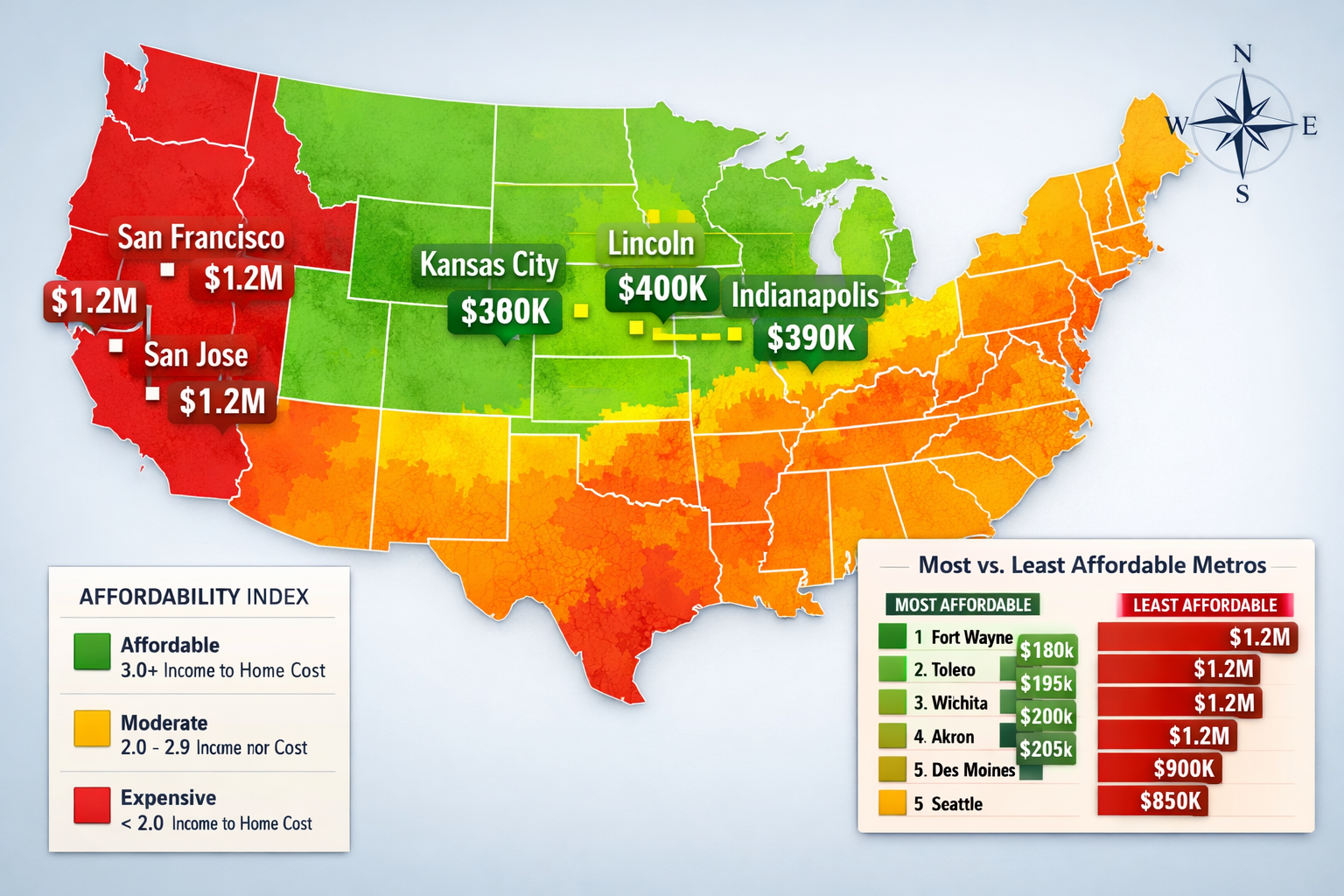

- Regional affordability varies dramatically: Midwest markets like Kansas City ($380,000 median) offer significantly better value than West Coast cities where San Jose requires 54% of household income for housing[1]

- Builder incentives remain widespread, with 65% of builders offering concessions and 36% cutting prices by an average of 6%[3]

- Home prices are stabilizing at near-zero growth for 2026, with median listing prices at $399,900 (down 0.1% year-over-year)[2][10]

- Month's supply of inventory is rising to 4.6 months, approaching balanced market conditions in many regions[2]

- Home prices impact affordability more than rates alone, requiring a comprehensive strategy beyond waiting for lower rates[5]

- First-time buyers should focus on emerging balanced markets in the Southeast and parts of Texas where bidding wars are declining[1]

Quick Answer

The 2026 housing affordability rebound is driven by mortgage rates falling from 7%+ to the low-6% range, combined with rising inventory and stabilizing home prices. This shift increases buyer purchasing power by 10-12% for each percentage point drop in rates, making homeownership accessible to households earning $94,000 or more in many markets. First-time buyers can maximize this opportunity by targeting regions with balanced inventory, negotiating builder incentives, and preparing strong financial profiles before rates potentially drop further in 2027.

How Much Do Falling Mortgage Rates Actually Improve Affordability?

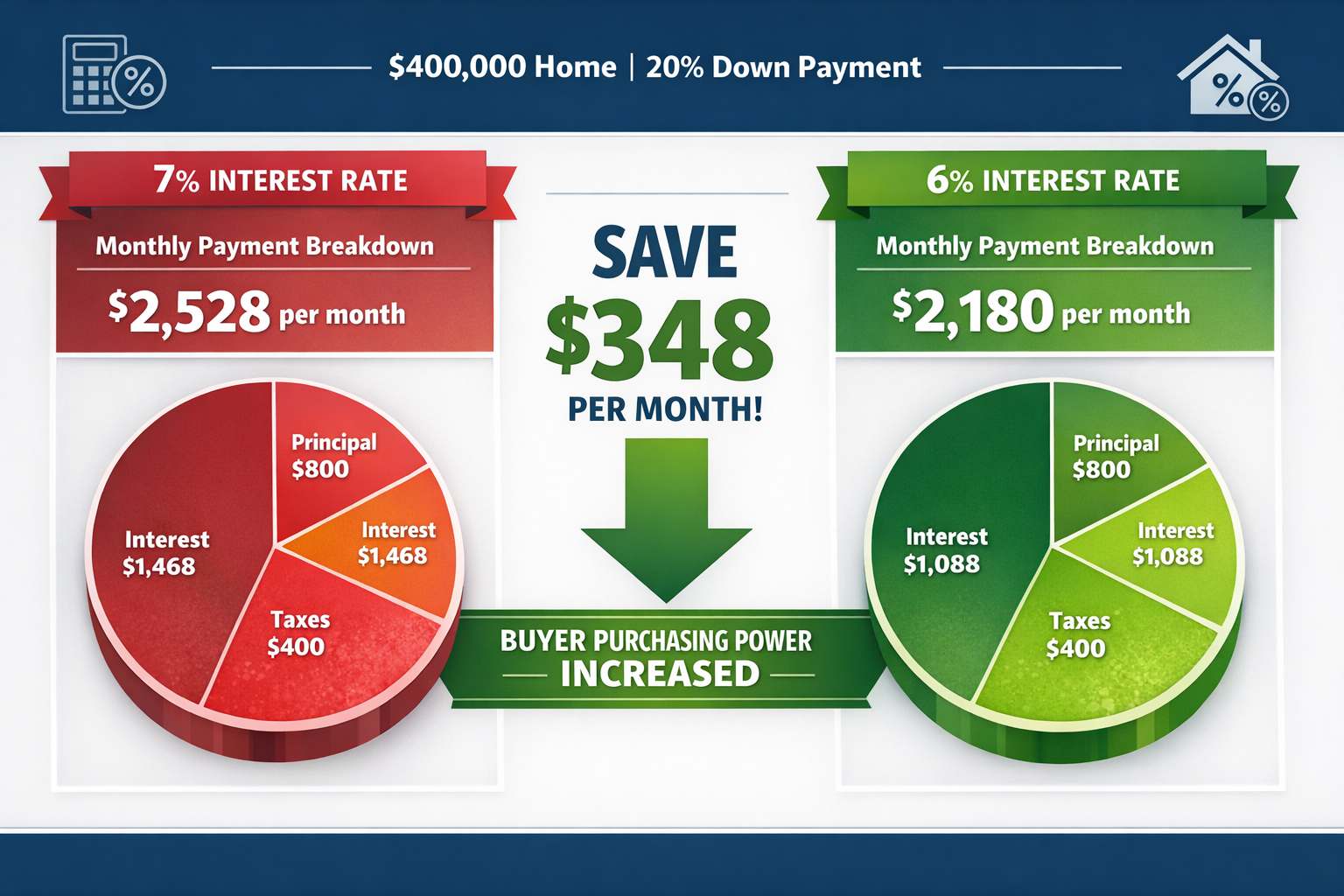

Falling mortgage rates directly increase buying power by reducing monthly payments, but the impact varies based on home price and down payment size. A drop from 7% to 6% on a $400,000 home with 20% down ($320,000 loan) reduces the monthly principal and interest payment by approximately $190, or about $2,280 annually.

Buying Power Comparison: 7% vs. 6% Rates

| Mortgage Rate | $400K Home (20% down) | Monthly P&I | Annual Savings vs. 7% | Equivalent Home Price at Same Payment |

|---|---|---|---|---|

| 7.0% | $320,000 loan | $2,129 | — | $400,000 |

| 6.5% | $320,000 loan | $2,022 | $1,284/year | $417,000 |

| 6.0% | $320,000 loan | $1,919 | $2,520/year | $435,000 |

| 5.5% | $320,000 loan | $1,817 | $3,744/year | $454,000 |

This table demonstrates that each 0.5% rate reduction allows buyers to afford approximately $17,000-$19,000 more in home value while maintaining the same monthly payment. For first-time buyers who have been saving during the high-rate period, this expanded purchasing power can mean the difference between qualifying for a starter home or remaining priced out.

Why Rates Alone Don't Solve the Affordability Crisis

Despite rate improvements, home prices remain the dominant affordability factor. According to recent analysis, mortgage rates would need to drop more than 4 percentage points from the current average of around 6.11% for typical homes to become fully affordable for median-income families[5]. The fundamental challenge stems from supply-demand imbalances, not just financing costs.

The income required to purchase a median-priced home has dropped from $103,000 one year ago to $94,000 as of February 2026[1], but this still exceeds the median household income in many markets. Buyers need to consider the complete affordability picture: home prices, local income levels, property taxes, insurance costs, and available inventory.

Common mistake: Waiting indefinitely for "perfect" rates while home prices appreciate can cost more than buying at slightly higher rates. Run the numbers for your specific market and timeline rather than following national rate predictions alone.

What Regional Markets Offer the Best Opportunities for First-Time Buyers in 2026?

The 2026 housing affordability rebound varies dramatically by region, with Midwest and select Southeast markets offering the strongest opportunities for first-time buyers. Markets with balanced inventory (4-6 months of supply), median prices below $400,000, and income-to-housing-cost ratios under 30% provide the most favorable conditions.

Most Affordable Major Markets for First-Time Buyers

Top opportunities (median home prices and income requirements):

- Kansas City, MO: $380,000 median price, moderate income requirements, growing inventory[1]

- Lincoln, NE: $389,000 median price, strong local economy, balanced market conditions[1]

- Indianapolis, IN: Similar price range, low property taxes, expanding job market

- Parts of Texas: Markets outside Austin showing balanced conditions with fewer bidding wars[1]

- Nashville and Atlanta suburbs: Shifting toward buyer-friendly conditions after years of rapid appreciation[1]

Markets to Approach with Caution

Challenging affordability (extreme income requirements):

- San Jose, CA: $1.195 million median (nearly 3x national median), requiring 54% of household income[1]

- Los Angeles, CA: Requiring 72% of median household income for typical home[1]

- San Francisco, CA: Similar extreme affordability challenges

- San Diego, CA: Coastal premium pricing with limited inventory relief

Decision rule: Choose Midwest or Southeast markets if you're a first-time buyer with household income between $75,000-$110,000. Consider these regions if you can work remotely or if your industry has strong presence there. Avoid West Coast markets unless your household income exceeds $150,000 or you have substantial down payment assistance.

Emerging Balanced Markets Worth Watching

Month's supply of inventory is expected to rise to 4.6 months nationally in 2026, within the 4-6 month range considered balanced[2]. Markets reaching this threshold show declining bidding wars, increased negotiating power for buyers, and price stabilization.

Atlanta, Nashville, and parts of Texas are transitioning from seller's markets to more balanced conditions[1]. These markets offer first-time buyers the advantage of selection without the frenzy of multiple offers above asking price that characterized 2021-2023.

How Can First-Time Buyers Calculate Their True Affordability in 2026?

True affordability extends beyond the mortgage payment to include property taxes, insurance, maintenance, HOA fees, and closing costs. First-time buyers should calculate total housing costs as a percentage of gross monthly income, targeting 28% or less for housing expenses and 36% or less for total debt obligations (the traditional 28/36 rule).

Complete Affordability Calculation Framework

Step 1: Calculate maximum monthly housing payment

- Gross monthly income × 28% = Maximum housing payment

- Example: $94,000 annual income ÷ 12 = $7,833/month × 28% = $2,193 maximum housing payment

Step 2: Subtract non-mortgage housing costs

- Property taxes (varies by location, typically 0.5-2.5% of home value annually)

- Homeowners insurance ($1,000-$3,000+ annually depending on location and coverage)

- HOA fees (if applicable, $100-$500+ monthly)

- PMI if down payment is less than 20% (typically 0.5-1% of loan amount annually)

- Maintenance reserve (budget 1% of home value annually)

Step 3: Determine affordable loan amount

- Use remaining monthly budget for principal and interest payment

- Apply current mortgage rate to calculate maximum loan amount

- Add down payment to determine total affordable home price

2026 Affordability Example

Household profile:

- Annual income: $94,000 (median required for current market)[1]

- Down payment saved: $30,000 (7.5%)

- Credit score: 720

- Current mortgage rate: 6.25%

Calculation:

- Maximum monthly housing: $7,833 × 28% = $2,193

- Estimated property tax: $400/month

- Homeowners insurance: $150/month

- PMI (less than 20% down): $180/month

- Available for P&I: $2,193 - $400 - $150 - $180 = $1,463

At 6.25% interest, a $1,463 monthly P&I payment supports approximately a $238,000 loan. Adding the $30,000 down payment yields a total affordable home price of $268,000.

Edge case: If rates drop to 5.5% by late 2026 or early 2027 as expected[2], the same $1,463 monthly payment would support a $257,000 loan, increasing total affordable price to $287,000—a $19,000 increase in buying power from rate improvement alone.

What Strategies Should First-Time Buyers Use to Maximize the 2026 Affordability Rebound?

First-time buyers can maximize the 2026 housing affordability rebound by combining rate timing with builder incentives, inventory leverage, and strategic market selection. The key is acting when local market conditions align favorably rather than waiting for perfect national conditions that may never materialize.

Proven Strategies for 2026 Market Conditions

1. Target builder inventory with incentives

Builder confidence remains low with the NAHB/Wells Fargo Housing Market Index at 36 in February 2026[3], creating opportunities for concessions. Currently, 65% of builders offer sales incentives, and 36% are cutting prices by an average of 6%[3].

Negotiable builder incentives include:

- Rate buydowns (builder pays points to reduce your rate by 0.5-1% for 1-3 years)

- Closing cost credits ($5,000-$15,000 common)

- Upgrades (flooring, appliances, landscaping)

- Price reductions (average 6% where offered)[3]

2. Get pre-approved before shopping

With inventory rising 8.9% in 2026[1], competition is easing but serious buyers still need pre-approval to negotiate effectively. Lenders are tightening standards, so demonstrate financial readiness early.

Pre-approval checklist:

- Credit score 620+ (640+ for better rates, 740+ for best rates)

- Debt-to-income ratio below 43% (lower is better)

- 2+ years employment history in same field

- Down payment funds seasoned in accounts for 60+ days

- Documentation ready: pay stubs, tax returns, bank statements

3. Focus on markets approaching balanced inventory

Month's supply reaching 4-6 months signals balanced conditions where buyers gain negotiating power[2]. Check local inventory trends monthly rather than relying on national averages.

4. Consider adjustable-rate mortgages (ARMs) if rates are expected to fall

If you plan to refinance when rates drop below 6% in 2027, a 5/1 or 7/1 ARM starting at 5.5-5.75% can reduce initial payments. Only choose this strategy if you have discipline to refinance and stable income to handle potential rate adjustments.

5. Expand search radius for affordability

With remote work still prevalent, consider markets within 30-60 minutes of job centers where prices drop 15-30%. This geographic flexibility can mean the difference between a $450,000 home and a $320,000 home with similar features.

Common mistake: Focusing exclusively on rate timing while ignoring inventory cycles. A home purchased at 6.5% in a buyer's market with 10% below asking price often beats waiting for 5.5% rates in a competitive market with bidding wars.

How Does Inventory Growth Impact First-Time Buyer Opportunities?

Rising inventory fundamentally shifts market dynamics from seller-dominated to balanced conditions, giving first-time buyers more selection, negotiating power, and time to make informed decisions. New listings rose 3.2% year-over-year nationally, and existing home inventory increased 15.2% in 2025 with an additional 8.9% growth expected in 2026[1][2].

What Inventory Growth Means for Buyers

Immediate benefits:

- More selection: Buyers can compare multiple properties rather than settling for the first acceptable option

- Reduced bidding wars: Markets approaching 4-6 months of supply see fewer multiple-offer situations[2]

- Negotiating leverage: Sellers become more willing to accept reasonable offers, cover closing costs, or make repairs

- Time to decide: Less pressure to make same-day offers without proper inspection or consideration

- Price stabilization: Median listing prices are down 0.1% year-over-year with 0% growth expected throughout 2026[2][10]

How to Use Inventory Data in Your Home Search

Monitor local month's supply metrics rather than just counting listings. Month's supply indicates how long it would take to sell all current inventory at the current sales pace:

- Less than 4 months: Seller's market, expect competition and bidding wars

- 4-6 months: Balanced market, reasonable negotiation possible

- More than 6 months: Buyer's market, significant negotiating power

Most real estate websites and local MLS reports publish month's supply data. Track this monthly in your target neighborhoods to identify when conditions shift in your favor.

Decision rule: If your target market shows 5+ months of supply and rising, you have strong negotiating position. Start with offers 5-8% below asking on properties listed more than 30 days. If supply is below 3 months, be prepared to offer at or slightly above asking on desirable properties.

What Are the Biggest Obstacles Still Facing First-Time Buyers in 2026?

Despite the 2026 housing affordability rebound, first-time buyers still face significant challenges including elevated home prices, down payment requirements, competition from cash buyers, and regional supply shortages. Understanding these obstacles helps buyers develop realistic strategies rather than expecting easy market entry.

Persistent Affordability Challenges

1. Home prices remain the dominant factor

While rates have improved, home prices have a bigger impact on affordability than mortgage rates alone[5]. The nationwide shortage of roughly 1.2 million housing units continues to constrain affordability improvements[2], keeping prices elevated even as demand moderates.

2. Down payment barriers

Even with falling rates, accumulating down payment funds remains challenging. A 20% down payment on a $400,000 home requires $80,000—years of savings for most first-time buyers. Options include:

- FHA loans (3.5% down, but requires mortgage insurance)

- Conventional 97 programs (3% down for qualified buyers)

- State and local first-time buyer assistance programs

- Gift funds from family members (properly documented)

3. Construction constraints limiting new supply

The residential construction sector faces nearly 300,000 job openings and needs to add roughly 740,000 workers annually to meet industry needs[2]. This labor shortage, combined with residential building material prices experiencing above-3% growth since June 2025[2], keeps new construction costs elevated and limits supply growth.

4. Regional income mismatches

In expensive markets, the gap between local median income and income required for homeownership remains severe. West Coast markets require 54-72% of household income for housing[1], far exceeding the traditional 28% guideline.

5. Credit and qualification standards

Lenders maintain stricter standards than pre-2008, requiring:

- Higher credit scores (680+ for conventional, 740+ for best rates)

- Lower debt-to-income ratios (preferably under 36%)

- Larger reserves (2-6 months of housing payments in savings)

- Stable employment history (2+ years same field)

Overcoming the Obstacles

Practical solutions for common barriers:

- Insufficient down payment: Explore 3-3.5% down payment programs, first-time buyer grants, or consider purchasing in lower-cost markets where 5-10% down is achievable

- Credit score below 680: Spend 6-12 months improving credit before applying—pay down credit card balances below 30% utilization, dispute errors, avoid new credit inquiries

- High debt-to-income ratio: Pay off smaller debts (car loans, credit cards) before applying, or increase income through side work documented on tax returns

- Priced out of preferred market: Expand geographic search, consider condos or townhomes as entry points, or wait for further rate declines while continuing to save

Edge case: Buyers with student loan debt face special DTI challenges. Federal student loans in income-driven repayment plans now use actual monthly payment (not 1% of balance) for qualification, potentially improving DTI ratios significantly.

When Is the Best Time to Buy in the 2026 Market Cycle?

The best time to buy in 2026 depends on local market conditions, your financial readiness, and rate expectations, but generally late spring through fall offers the most inventory selection while winter provides less competition. With rates expected to remain in the low-6% range throughout most of 2026 before potentially dropping below 6% in 2027[2], timing your purchase requires balancing rate expectations against inventory availability and personal readiness.

Seasonal Timing Considerations

Spring (March-May):

- Pros: Peak inventory, most selection, sellers motivated to list

- Cons: Most competition from other buyers, higher prices

- Best for: Buyers who need maximum selection and want to move during summer

Summer (June-August):

- Pros: Still strong inventory, families motivated to close before school year

- Cons: Competition remains elevated, hot weather for house hunting

- Best for: Buyers with school-age children needing summer move-in

Fall (September-November):

- Pros: Motivated sellers who didn't sell in spring/summer, less competition

- Cons: Declining inventory, weather considerations for inspections

- Best for: Flexible buyers seeking negotiating leverage

Winter (December-February):

- Pros: Least competition, most motivated sellers, potential price concessions

- Cons: Limited inventory, holiday disruptions, weather challenges

- Best for: Buyers ready to act quickly on limited inventory with strong negotiating position

Rate Timing Strategy for 2026-2027

Current rates in the low-6% range are not expected to drop below 6% until 2027[2]. This creates a strategic decision: buy now at 6-6.5% and refinance later, or wait for lower rates while continuing to rent.

Buy now if:

- You find a home meeting your needs in your budget

- Local inventory is rising and giving you negotiating power

- Rent increases are offsetting potential savings from waiting

- You can afford the payment at current rates

- You plan to refinance when rates drop below 6%

Wait if:

- You're not financially ready (credit score below 640, insufficient down payment)

- Your target market is still showing seller's market conditions

- You have a favorable rent situation with minimal increases

- Your income or employment situation is uncertain

- You're hoping for specific properties not yet on market

Calculation to make the decision: Compare 12 months of rent payments plus continued savings to the cost of buying now and refinancing in 12-18 months when rates drop. Include closing costs for both purchase and refinance. Often buying sooner wins even with a refinance cost because you're building equity and locking in a price rather than risking appreciation.

What First-Time Buyer Programs and Incentives Are Available in 2026?

First-time buyers in 2026 can access federal, state, and local programs offering down payment assistance, reduced interest rates, tax credits, and favorable loan terms. These programs significantly improve affordability but require research and often have income limits, geographic restrictions, and education requirements.

Federal Programs for First-Time Buyers

FHA Loans:

- 3.5% down payment minimum

- Credit scores as low as 580 accepted (500-579 with 10% down)

- Mortgage insurance required (both upfront and monthly)

- Loan limits vary by county (up to $498,257 in most areas, higher in expensive markets)

- Best for buyers with limited down payment and credit scores below 680

VA Loans (for veterans and active military):

- 0% down payment

- No mortgage insurance

- Competitive interest rates

- Funding fee required (can be financed)

- Best for eligible veterans and service members

USDA Loans (for rural and suburban areas):

- 0% down payment

- Income limits apply (typically 115% of area median income)

- Property must be in USDA-eligible area (many suburbs qualify)

- Guarantee fee required

- Best for buyers in qualifying areas with moderate income

Conventional 97 and HomeReady/Home Possible:

- 3% down payment

- First-time buyer or low-to-moderate income requirements

- Mortgage insurance required but can be removed at 80% LTV

- Competitive rates for good credit (680+)

- Best for buyers with good credit but limited down payment

State and Local Down Payment Assistance Programs

Most states offer down payment assistance ranging from $2,500 to $25,000+ through grants, forgivable loans, or deferred-payment second mortgages. Common structures include:

- Grants: Free money that doesn't need to be repaid (often $5,000-$15,000)

- Forgivable loans: Loans forgiven after living in home for specified period (typically 5-10 years)

- Deferred second mortgages: No monthly payment, due when you sell or refinance

- Matched savings programs: State matches your savings contributions

Typical eligibility requirements:

- First-time buyer (or haven't owned home in 3+ years)

- Income limits (usually 80-120% of area median income)

- Purchase price limits

- Homebuyer education course completion

- Primary residence requirement

- Minimum occupancy period (usually 3-5 years)

How to find programs: Contact your state housing finance agency, check with local housing authorities, or ask lenders about available programs in your area. Many programs are under-utilized because buyers don't know they exist.

How Should First-Time Buyers Prepare Financially for the 2026 Market?

Financial preparation for first-time buyers in 2026 requires building credit, accumulating down payment and closing costs, reducing debt, and establishing emergency reserves beyond the home purchase. Start preparation 12-18 months before your target purchase date to maximize qualification and negotiating position.

12-18 Month Preparation Timeline

Months 12-18 before purchase:

- Pull credit reports from all three bureaus (free at AnnualCreditReport.com)

- Dispute any errors and begin credit improvement plan

- Create dedicated savings account for down payment and closing costs

- Research target markets and price ranges

- Calculate realistic budget using 28/36 rule

- Begin tracking housing market conditions in target areas

Months 6-12 before purchase:

- Increase credit score to 680+ (740+ for best rates)

- Accelerate down payment savings (automate transfers)

- Pay down high-interest debt to improve DTI ratio

- Avoid major purchases or new credit accounts

- Research first-time buyer programs and assistance

- Complete homebuyer education course (often required for assistance programs)

- Gather financial documentation (tax returns, pay stubs, bank statements)

Months 3-6 before purchase:

- Get pre-approved with 2-3 lenders to compare rates and terms

- Finalize down payment amount (keep funds in accounts for 60+ days seasoning)

- Select real estate agent experienced with first-time buyers

- Begin active house hunting in target neighborhoods

- Attend open houses to refine preferences

- Monitor mortgage rates weekly

Months 1-3 before purchase:

- Intensify house search when market conditions align

- Make offers on suitable properties

- Complete home inspection and negotiate repairs

- Finalize mortgage application and lock rate

- Conduct final walkthrough

- Close on home

Essential Financial Benchmarks

Credit score targets:

- 620: Minimum for most conventional loans

- 640: Better rate options open up

- 680: Good rates, more program options

- 740+: Best rates and terms available

Down payment targets:

- 3-3.5%: Minimum for many programs, requires mortgage insurance

- 5-10%: Reduces monthly MI cost, shows stronger financial position

- 20%: Eliminates mortgage insurance, best rates, strongest offers

Savings beyond down payment:

- Closing costs: 2-5% of purchase price ($8,000-$20,000 on $400,000 home)

- Moving expenses: $1,000-$5,000 depending on distance and amount

- Immediate repairs/improvements: $2,000-$10,000 for unexpected issues

- Emergency fund: 3-6 months expenses (including new housing payment)

Debt-to-income targets:

- 36% or less: Traditional lending standard, best approval odds

- 43%: Maximum for most conventional loans

- Under 50%: FHA maximum with compensating factors

Common mistake: Draining all savings for down payment and closing costs, leaving no emergency fund. Always maintain at least $5,000-$10,000 in reserves after closing for unexpected repairs, job loss, or other emergencies.

Frequently Asked Questions

Q: Will mortgage rates drop below 6% in 2026? Sustained rates below 6% are not expected until 2027, though temporary dips below 6% may occur in late 2026[2]. Current forecasts show rates remaining in the low-6% range throughout most of 2026.

Q: How much does a 1% rate drop save on a monthly mortgage payment? On a $320,000 loan (typical for $400,000 home with 20% down), a 1% rate drop from 7% to 6% saves approximately $190 per month or $2,280 annually in principal and interest payments.

Q: Should I wait for lower rates or buy now and refinance later? Buy now if you find a suitable home at a price you can afford and your local market shows rising inventory or balanced conditions. You can refinance when rates drop, but waiting risks home price appreciation that could offset rate savings.

Q: What credit score do I need to buy a home in 2026? Minimum scores are 580 for FHA loans (500 with 10% down) and 620 for conventional loans, but scores of 680+ access better rates and 740+ receive the best terms available.

Q: How much down payment do I need as a first-time buyer? Minimum down payments range from 0% (VA, USDA) to 3-3.5% (FHA, Conventional 97), though 20% down eliminates mortgage insurance and strengthens your offer. Most first-time buyers put down 5-10%.

Q: What is the median home price in 2026? The national median listing price for existing homes was $399,900 in January 2026, down 0.1% from the previous year, with prices expected to remain flat throughout 2026[2][10].

Q: What income do I need to buy a home in 2026? The income required to purchase a median-priced home nationally fell to $94,000 as of February 2026[1], though this varies significantly by region—from under $70,000 in affordable Midwest markets to $150,000+ in expensive coastal cities.

Q: Are home prices falling in 2026? Home prices are stabilizing rather than falling significantly, with 0% growth expected throughout 2026[2][10]. Some markets show modest declines while others see slight appreciation, but dramatic price drops are not occurring nationally.

Q: What are builder incentives and how do I negotiate them? Builder incentives include rate buydowns, closing cost credits, upgrades, and price reductions. Currently 65% of builders offer incentives and 36% are cutting prices by an average of 6%[3]. Negotiate by comparing multiple builders, asking specifically about available concessions, and being ready to commit when favorable terms are offered.

Q: How long does the home buying process take? From pre-approval to closing typically takes 60-90 days, including 30-45 days for house hunting, 7-14 days for offer acceptance and inspection, and 30-45 days for mortgage underwriting and closing.

Q: Should I buy a condo or house as a first-time buyer? Condos typically cost 15-30% less than single-family homes in the same area, making them good entry points for first-time buyers. Consider condos if you want lower maintenance, can accept HOA fees and rules, and plan to upgrade to a house within 5-10 years. Choose houses if you want more control, privacy, and long-term appreciation potential.

Q: What is mortgage insurance and how much does it cost? Mortgage insurance protects the lender if you default and is required when down payment is less than 20%. FHA mortgage insurance costs 0.55-0.85% of loan amount annually plus 1.75% upfront. Conventional PMI costs 0.5-1% annually and can be removed when you reach 80% loan-to-value through payments or appreciation.

Conclusion

The 2026 housing affordability rebound represents a genuine opportunity for first-time buyers who have been sidelined by high rates and competitive conditions in recent years. With mortgage rates falling from 7%+ to the low-6% range, inventory rising 8.9% in 2026, and home prices stabilizing at near-zero growth, market dynamics are shifting toward more balanced conditions that favor prepared buyers.

The key to success in this market is recognizing that affordability improvements are gradual and regional rather than dramatic and universal. First-time buyers should focus on markets approaching 4-6 months of inventory supply, target builder inventory with incentives, and prepare strong financial profiles with credit scores above 680 and down payments of at least 5-10%.

While challenges remain—including elevated home prices, regional supply shortages, and income mismatches in expensive markets—the combination of falling rates, rising inventory, and widespread builder concessions creates the best entry conditions since 2020. Buyers who act strategically when local conditions align, rather than waiting for perfect national conditions, will position themselves to build equity and benefit from future rate declines through refinancing.

Actionable Next Steps

- Calculate your true affordability using the complete framework including taxes, insurance, and reserves

- Check your credit score and begin improvement plan if below 680

- Research your target market's inventory trends monthly to identify balanced conditions

- Get pre-approved with 2-3 lenders to compare rates and understand your buying power

- Explore first-time buyer programs through your state housing finance agency

- Identify 3-5 target neighborhoods within your budget and monitor new listings

- Build emergency fund to maintain 3-6 months expenses after closing

- Complete homebuyer education course to qualify for assistance programs

- Interview real estate agents experienced with first-time buyers in your market

- Create action timeline based on your financial readiness and local market conditions

The 2026 housing affordability rebound is real, but it rewards buyers who combine financial preparation with strategic market timing. Start your preparation today to position yourself for homeownership when conditions in your target market align favorably.

References

[1] February 2026 Real Estate Market Update Forecast - https://www.churchillmortgage.com/articles/february-2026-real-estate-market-update-forecast?hs_amp=true

[2] 2026 Housing Outlook Ongoing Challenges Cautious Optimism And Incremental Gains - https://www.nahb.org/news-and-economics/press-releases/2026/02/2026-housing-outlook-ongoing-challenges-cautious-optimism-and-incremental-gains

[3] Builder Sentiment Edges Lower On Affordability Concerns - https://www.nahb.org/news-and-economics/press-releases/2026/02/builder-sentiment-edges-lower-on-affordability-concerns

[5] Housing Affordability In 2026 Why Rates Are Not The Only Factor - https://www.pointmtg.com/blog/housing-affordability-in-2026-why-rates-are-not-the-only-factor

[10] Us Housing Market Outlook - https://www.jpmorgan.com/insights/global-research/real-estate/us-housing-market-outlook